ChatGPT Can Now See Your Bank Account: OpenAI Launches Personal Finance Tool — and Controversy Erupts

There is a psychological threshold that many people had not yet crossed with artificial intelligence. Telling it your problems, entrusting it with writing work emails, using it for programming or research: all acceptable. But showing an AI your current account, your transactions, your investments, your debts? This is different territory. OpenAI knows this, and on May 15, 2026, it decided to enter anyway with the official launch of ChatGPT Finances — a personal finance tool integrated directly into ChatGPT, allowing users to connect their bank accounts, credit cards, and investment portfolios to the AI. Reactions were immediate.

The operation is technically straightforward. From the ChatGPT interface — web or iOS — you open the Finances section from the sidebar and start the connection process. The system uses Plaid as the connection infrastructure: anyone who has ever used fintech services like Robinhood, Venmo, or any budgeting app already knows Plaid, even without knowing it. It is the system that acts as a bridge between applications and actual banking data, and it is used by practically the entire American fintech sector.

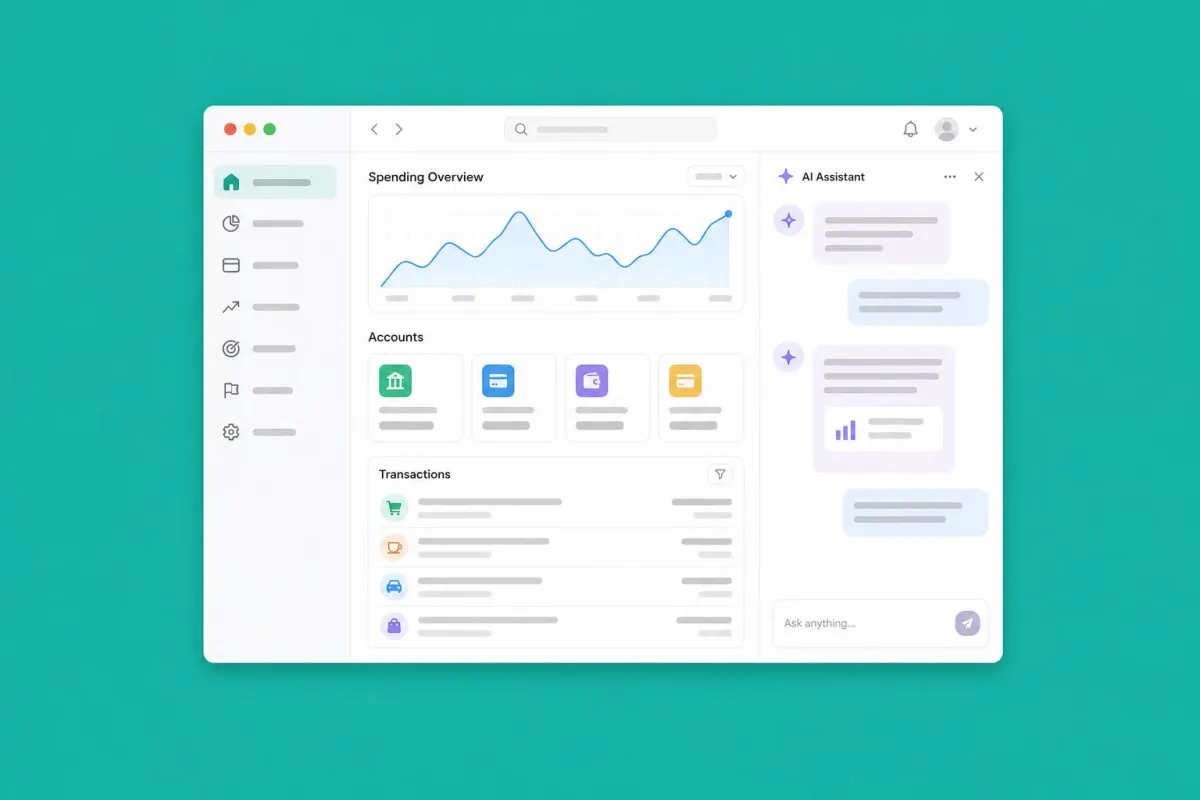

Once authenticated, ChatGPT begins to synchronize and categorize financial data. The result is a comprehensive dashboard that shows at a glance the user's financial situation: investment portfolio performance, expenses categorized by type, active subscriptions, payments due in the coming days, and balances of current accounts and credit cards. Coverage is enormous: over 12,000 supported financial institutions, including Chase, Bank of America, Fidelity, Schwab, Robinhood, American Express, and Capital One.

The point OpenAI emphasizes strongly is that the connection is strictly read-only. ChatGPT cannot move money, cannot initiate payments, and cannot modify anything on the connected accounts. This constraint is imposed at the Plaid infrastructure level, not just as a matter of policy. The AI sees, analyzes, responds — but does not act.

The real value proposition is not the dashboard itself — tools like Mint, YNAB or services integrated into banking apps have been doing similar things for years. The value is the conversation. You can ask ChatGPT to analyze your spending over the last quarter and identify where you are spending more than expected. You can ask it to compare your current investments with your stated goals. You can ask it when you will be able to save a certain amount taking into account your actual cash flow, not a generic estimate.

The difference compared to any previous app-based financial advisor is that the reasoning occurs in natural language, with real and updated data, and can be explored in an iterative way. You don't get a pre-packaged answer based on predefined categories. You get a contextual analysis based on your specific numbers, with the ability to follow up, ask for alternative scenarios, and explore implications you hadn't considered.

GPT-5.5, the model powering ChatGPT Pro, has quantitative and contextual reasoning capabilities significantly superior to previous models. This means that financial analyses are not simple sums and averages: the model can identify patterns, anomalies, correlations between spending behaviors and specific periods, and reason on future projections with a level of sophistication that goes far beyond standard pie charts.

For now, the tool is available in preview exclusively for ChatGPT Pro users in the United States. ChatGPT Pro costs 200 dollars per month — OpenAI's highest-tier plan. OpenAI has stated its intention to extend the tool to the Plus plan and subsequently to the free plan, but without providing precise timelines. There are currently no indications of when — and if — it will arrive in Europe, where financial and privacy regulations pose significantly more stringent constraints than in the United States.

OpenAI has explicitly communicated that financial data connected through the Plaid integration is not used to train AI models. Users can disconnect accounts at any time from the settings, view and delete financial memories associated with conversations, and use temporary chats that are not saved in the history. Once an account is disconnected, synchronized data is removed from ChatGPT within 30 days.

Plaid, for its part, uses AES-256 encryption — the banking standard — and operates under current financial regulations in the United States. On a technical level, the infrastructure is the same already used by millions of fintech users every day.

The launch has generated a heated debate, and the criticisms are multiple and come from different directions.

The most immediate and widespread criticism is that of trust. OpenAI is a company that has had, over the last few years, several controversial episodes related to the management of user data and its policies. Entrusting it with complete visibility into one’s financial life — transactions, balances, investments, debts — is a step that many users and analysts judge premature.

The fact that data is not used for training is a policy statement, not a structural technical guarantee. Policies change. Companies are acquired. Terms of service are updated. Those who connect their bank accounts today have no guarantees on how this data will be managed in two years, when OpenAI's corporate conditions could be very different from current ones.

A second line of criticism concerns the quality of responses. Language models hallucinate — they produce plausible but incorrect information with a frequency that, in many contexts, is acceptable. In a financial context, however, a hallucination can have concrete and serious consequences. If ChatGPT analyzes your spending and tells you that you are saving when in reality you are going into the red, or provides you with incorrect projections upon which you base real investment decisions, the damage is not just informational.

OpenAI does not position itself as a regulated financial advisory service, and specifies this in its terms of service. But the conversational mode in which the tool presents its analyses can lead users to treat responses as professional advice, even when they are not. The difference between an analysis tool and an advisor is much subtler in a chat interface than in a legal disclaimer that no one reads.

OpenAI pays Plaid for financial connections — a significant cost at scale. If financial data is not used for training and is not sold to third parties, how is this service economically sustained? The most obvious answer is that the tool serves to make ChatGPT Pro indispensable, increasing the retention rate and justifying the 200 dollars per month price tag. But this logic implies that financial data is creating economic value for OpenAI in some form — even if not through direct sale. In such a sensitive area, opacity generates legitimate concern.

According to reports from several sources, class-action filings already exist alleging previous episodes of improper data sharing by OpenAI. These proceedings precede the launch of ChatGPT Finances, but add a legal context that makes the issue of trust in financial data even more delicate and controversial.

For now, the tool is only available in the United States, and that is no coincidence. In Europe, the combination of GDPR and financial regulations like PSD2 — which regulates access to banking data by third parties — makes the legitimacy of a service like this in its current form much more complex. Several European legal experts have already commented that the consent and data management model presented by OpenAI might not comply with European Union regulations without significant structural changes. For Italian and European users, therefore, the wait could be long — and not just for commercial reasons.

Beyond the controversies, ChatGPT Finances is a very clear signal of where AI is headed in the medium term. An AI that knows your real financial situation, your goals, your spending behavior, and your investments has the necessary information to become a full-fledged personal financial advisor — something that until recently was accessible only to those with enough wealth to justify a private banker. This democratization of financial advice is genuinely valuable, especially for those who have never had access to professional management of their money.

The next step — which OpenAI has not yet announced but which many analysts consider inevitable — is the move toward action: not just seeing and analyzing, but executing. Paying bills, rebalancing portfolios, optimizing subscriptions, negotiating rates. When financial AI moves from reading to writing, questions about trust, security, and regulation will no longer be academic. They will be urgent.

For now, ChatGPT Finances is a tool that offers something real to those willing to surrender a level of visibility into their financial data that until yesterday we would have considered reserved exclusively for one's bank. Whether that surrender is worth the value received is a decision that every user must make independently — with full awareness of what they are sharing and with whom.